|

|

|

[Majorityrights Central] Three possible forms of a Ukrainian victory ... and a Russian defeat Posted by Guessedworker on Thursday, 16 April 2026 16:36. [Majorityrights Central] “If America doesn’t learn ...” Posted by Guessedworker on Sunday, 22 March 2026 17:52. [Majorityrights News] Gerdes on the possible sea-change in the Ukraine War? Posted by Guessedworker on Friday, 20 March 2026 21:45. [Majorityrights Central] Some intel on the Islamic Revolutionary Guards Corps Posted by Guessedworker on Thursday, 12 March 2026 23:32. [Majorityrights Central] Defining the borders of the English kin-group Posted by Guessedworker on Wednesday, 11 March 2026 23:51. [Majorityrights News] Jason Jay Smart on the approaching collapse of Putin’s reign Posted by Guessedworker on Wednesday, 11 March 2026 22:42. [Majorityrights Central] Empires, the Chinese Mind, a theoretical nationalism of ethnicity Posted by Guessedworker on Saturday, 14 February 2026 01:54. [Majorityrights Central] Gemini - not an identical twin to ChatGTP Posted by Guessedworker on Friday, 06 February 2026 16:58. [Majorityrights News] Warburg on the impact of Russian forces’ loss of access to Starlink Posted by Guessedworker on Friday, 06 February 2026 10:17. [Majorityrights News] Toast à la Little Saint James Posted by Guessedworker on Wednesday, 04 February 2026 23:48. [Majorityrights News] Southport, migrant hotels, the national flag, and Amelia Posted by Guessedworker on Monday, 02 February 2026 00:14. [Majorityrights Central] Argot Rosetta Stone For GW/Heidegger/Etter Posted by James Bowery on Saturday, 31 January 2026 17:18. [Majorityrights Central] ChatGPT redux Posted by Guessedworker on Thursday, 29 January 2026 01:11. [Majorityrights News] The national revolution in Iran cannot be stopped Posted by Guessedworker on Saturday, 10 January 2026 00:38. [Majorityrights Central] Into the authoritarian world redux Posted by Guessedworker on Saturday, 03 January 2026 17:56. [Majorityrights News] Moscow Times: Valdai residents report no sign of drones attacking Putin residence Posted by Guessedworker on Tuesday, 30 December 2025 11:33. [Majorityrights News] Paul Warburg on America’s self-destructive new strategy Posted by Guessedworker on Tuesday, 16 December 2025 12:32. [Majorityrights Central] Thoughts on Mark Collett’s strategy for nationalism in the British future Posted by Guessedworker on Friday, 24 October 2025 15:01. [Majorityrights Central] Living in the Jewish Mind: Part One Posted by Guessedworker on Monday, 29 September 2025 09:37. [Majorityrights News] Nationalism on the Kramatorsk front. Posted by Guessedworker on Saturday, 20 September 2025 15:55. [Majorityrights Central] And Chat GPT just the same Posted by Guessedworker on Monday, 08 September 2025 15:18. [Majorityrights Central] Grok the modern nationalist Posted by Guessedworker on Sunday, 07 September 2025 19:14. [Majorityrights Central] Principles, parts, processes of ethnic nationalism, Part 1: inflection? Posted by Guessedworker on Thursday, 31 July 2025 12:03. [Majorityrights Central] A window onto a world of Russo-Chinese hegemony Posted by Guessedworker on Tuesday, 08 July 2025 20:47. [Majorityrights Central] The DT takes the first step on the journey Posted by Guessedworker on Thursday, 03 July 2025 05:02. [Majorityrights News] Iranian comment machine switched off by Israeli bombs Posted by Guessedworker on Wednesday, 25 June 2025 09:07. [Majorityrights Central] After Casey and the ensuing child sexual exploitation inquiry Posted by Guessedworker on Tuesday, 17 June 2025 00:21. [Majorityrights News] 4 minutes and 43 seconds of drone warfare history - updated Posted by Guessedworker on Wednesday, 04 June 2025 16:50. [Majorityrights Central] An approaching moment of Russian clarity Posted by Guessedworker on Sunday, 11 May 2025 12:34. [Majorityrights Central] “It’s started. You ignored us. See where it’s going to get you.” Posted by Guessedworker on Sunday, 04 May 2025 00:42. [Majorityrights News] Another dramatic degradation of Russia’s combat capacity Posted by Guessedworker on Wednesday, 23 April 2025 08:49. [Majorityrights Central] A British woman in Ukraine and an observer of Putin’s war Posted by Guessedworker on Monday, 14 April 2025 00:04. [Majorityrights News] France24 puts an end to Moscow’s lie about the attack on Kryvyi Riy Posted by Guessedworker on Monday, 07 April 2025 17:02. [Majorityrights News] If this is an inflection point Posted by Guessedworker on Thursday, 03 April 2025 05:10. Majorityrights News > Category: World Affairs

Caveat: The numbers on some countries do NOT appear to be updated - particularly not for China.

Related:

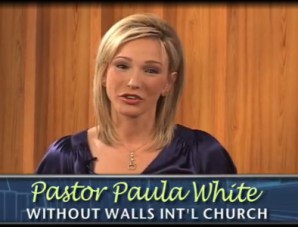

...TweetsHemant Mehta@hemantmehta 7:23 PM · Mar 17, 2020 Trump’s “spiritual adviser” (and head of the White House’s “Faith and Opportunity Initiative” program) Paula White asked for cash during a coronavirus-related prayer session this afternoon: “Maybe you’d like to sow a $91 seed… Or maybe $9. Or whatever God tells you to do.”

Not content with being “the new Cyrus” it appears Trump also wants to be the new James I and own the title of “the wisest fool in Christendom”. - mancinblack

Page 10 of 62 | First Page | Previous Page | [ 8 ] [ 9 ] [ 10 ] [ 11 ] [ 12 ] | Next Page | Last Page |

|

Existential IssuesDNA NationsCategoriesContributorsEach author's name links to a list of all articles posted by the writer. LinksEndorsement not implied. Immigration

Islamist Threat

Anti-white Media Networks Audio/Video

Crime

Economics

Education General

Historical Re-Evaluation Controlled Opposition

Nationalist Political Parties

Science Europeans in Africa

Of Note MR Central & NewsCommentsThorn commented in entry 'Trout Mask Replica' on Wed, 04 Feb 2026 00:45. (View) Thorn commented in entry 'Slaying The Dragon' on Tue, 03 Feb 2026 23:41. (View) Guessedworker commented in entry 'Slaying The Dragon' on Sun, 01 Feb 2026 18:47. (View) James Bowery commented in entry 'Slaying The Dragon' on Sun, 01 Feb 2026 17:55. (View) Thorn commented in entry 'Slaying The Dragon' on Sun, 01 Feb 2026 00:30. (View) James Bowery commented in entry 'Slaying The Dragon' on Sat, 31 Jan 2026 22:12. (View) Guessedworker commented in entry 'ChatGPT redux' on Sat, 31 Jan 2026 09:59. (View) James Bowery commented in entry 'ChatGPT redux' on Fri, 30 Jan 2026 21:26. (View) Thorn commented in entry 'Into the authoritarian world redux' on Fri, 30 Jan 2026 14:17. (View)  |

Will Trump’s appeal to Christian Zionist base cull

Will Trump’s appeal to Christian Zionist base cull